The “Money Sunday” Routine That Quietly Fixed My Chaotic Finances

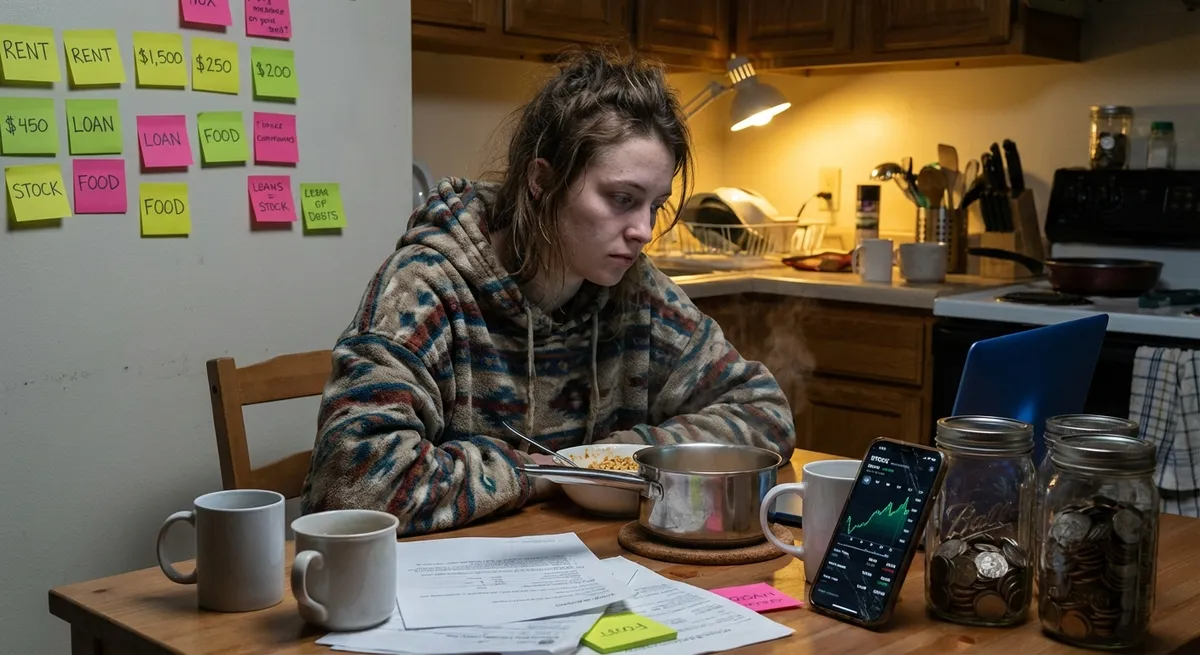

I used to treat my money like a bad group chat: I’d mute it, ignore it, and hope it just…sorted itself out. Spoiler: it didn’t. I was making decent money and still feeling broke, constantly blindsided by random charges, “surprise” renewals, and that one friend who always wants to split the birthday dinner “evenly.”

Then I accidentally stumbled into a habit that completely flipped how I handle money: a 45–60 minute “Money Sunday” routine. It’s not budgeting in the stiff, spreadsheet way. It’s more like a weekly vibe check with my bank accounts. When I tested this for a month, my stress dropped so hard it was almost suspicious. Three months in, I’d paid off a lingering card balance, stopped overdrafting, and finally knew where my cash was actually going.

Here’s exactly how I run it, what worked, what backfired, and how you can steal the parts that fit your life.

Why I Needed a Weekly Money Ritual (Not a Giant Life Overhaul)

For years, I tried to “get my finances together” with massive, unsustainable efforts. One weekend I’d build a color‑coded budget with 19 categories and a savings plan that assumed I’d never touch DoorDash again. By Tuesday, that budget was a fossil.

The problem wasn’t knowledge. I’d read all the classics—Ramit Sethi, Your Money or Your Life, the FIRE blogs. I knew the terms: emergency fund, index funds, expense ratios, compound interest. But there’s a huge gap between knowing and checking your account before you tap Apple Pay for the third time in a day.

What finally clicked for me was hearing a CFP (certified financial planner) say in a podcast that “money is a behavior system, not a math problem.” I felt weirdly called out. The math wasn’t what was breaking; my habits were.

So I tried something tiny: every Sunday, before I opened Netflix, I’d sit down with my laptop and phone and look at my money—no spreadsheets, no judgment, just a weekly “where are we?” check‑in. That single habit did more for my finances than any New Year’s resolution I’ve ever made.

Here’s how my “Money Sunday” is set up now and how you can customize your own version.

Step 1: The 10‑Minute “Reality Snapshot” (a.k.a. No More Money Ghosting)

The first part of my routine is basically ripping off the Band‑Aid: I look at everything I was avoiding all week.

I open three things, always in the same order:

- Checking account

- Credit cards

- Savings and investments

I don’t analyze yet; I’m just looking. When I first started, this part alone made me want to yeet my phone into a lake. I’d see charges I forgot about, subscriptions I didn’t remember starting, and my “fun” spending looking suspiciously like mild chaos.

What I track in these 10 minutes:

- Current balances – How much cash is in checking vs. what bills are coming up.

- Upcoming automatic payments – Especially rent/mortgage, utilities, and card due dates.

- Weird or surprising charges – Anything I don’t recognize or regret instantly.

The first month, I caught:

- A $21.99 subscription I thought I canceled six months earlier.

- A “free trial” that quietly converted to $12.99/month.

- A random foreign charge that turned out to be fraud (my bank reversed it).

That last one alone made this routine worth it. According to the Federal Trade Commission, credit card fraud reports jumped sharply in the last decade, with millions of cases reported annually in the U.S. alone. Catching weird charges early gives you a much better shot at getting your money back.

The rule I use: if I don’t recognize a transaction within 15 seconds, I bookmark it and investigate. No spiraling, just treating it like a detective job.

Step 2: The 20‑Minute “Past Week Autopsy” (Where Your Patterns Get Busted)

Once I know the raw numbers, I spend about 20 minutes asking: How did my money actually behave this week?

When I tested this, I tried both manual tracking and apps. Here’s what I learned:

- Apps like Mint (RIP), Monarch Money, YNAB, and Empower are great at automatic categorization, but they sometimes mis‑label stuff (my favorite coffee shop kept showing up as “travel”).

- Manual tracking in a simple Google Sheet felt annoying at first but weirdly made me “feel” every purchase in a good way.

Now I use a hybrid: my card and bank apps for categorization, plus a really simple note in my phone where I jot down “extra” spending that I know isn’t essential (takeout, random Target runs, impulse Amazon buys).

During the autopsy part, I ask:

- Did I spend roughly what I expected on food, transport, fun?

- Were there “emotion purchases” (stress, boredom, social pressure)?

- What would I honestly cut next week without making my life miserable?

One week I realized I’d ordered delivery four times purely because I didn’t want to wash dishes. That was about $120—almost a full extra payment on my highest‑interest card. Seeing it as a lump instead of “just $25 here, $30 there” was brutal but clarifying.

I don’t punish myself; I just tag it. “Okay, that was a stress week. Good to know. How do we plan around that next time?”

A detail I stole from behavioral economics research: I created “friction” around my problem categories. Since I know food delivery is my weakness, I:

- Deleted my card from the delivery apps so I have to re‑type it.

- Moved delivery apps to a folder on the last screen of my phone.

- Set a rule: delivery only if I’ve already cooked at home twice this week.

That little bit of friction, backed by weekly reviews, genuinely cut my delivery spending by about 40% over two months.

Step 3: The 10‑Minute “Future Week Blueprint” (Pre-Deciding So You Don’t Panic-Spend)

The next part is where this routine stops being “painful accounting” and starts being calming.

I shift from “what happened?” to “what’s coming up?”

I look at my calendar and ask:

- Do I have any social plans that will cost money? (dinners, birthdays, trips)

- Any one‑off “adulting” hits? (car service, copays, renewals, gifts)

- Any income changes? (extra gig, freelance payment, or a slower week)

Then I create a super simple plan for just the next seven days. I’m not forecasting my life for 12 months; I’m getting through the next week with intention.

Very rough example of what I’ll write in my notes app:

- “This week: two dinners out, one coffee date, gym payment, streaming renewals.”

- “Cap eating out at $80 total.”

- “Transfer $100 extra to card if freelance invoice lands by Thursday.”

When I consistently did this for eight weeks, I noticed something important: I wasn’t “good with money” or “bad with money”—I was either pre‑deciding or winging it. Pre‑deciding won almost every time.

Research backs this up. Behavioral economists talk about “implementation intentions” — basically, specific “if X, then Y” plans. Studies show that when people pre‑commit to certain actions with clear triggers, they’re far more likely to follow through, including on financial decisions.

So I’ll literally write: “If I get invited out more than twice this week, I say yes only if it’s under $30 or I already have cash set aside.”

That sounds dorky on paper, but when I’ve already made that rule on Sunday, it’s way easier to say, “I’m sitting this one out” on Friday night without feeling like the broke friend.

Step 4: The 5‑Minute “Tiny Wealth Move” (Where the Long-Term Magic Hides)

This is the sneaky part that quietly changed my net worth: every Money Sunday, I do one small thing that benefits Future Me.

It’s never huge. I’m not maxing out a Roth IRA in one sitting. It’s micro‑moves like:

- Increasing my automatic 401(k) contribution by 1% after a raise.

- Rounding up my weekly debt payment by $15.

- Moving an extra $20–$50 into a high‑yield savings account.

- Checking my investment allocation is still mostly low‑cost index funds.

When I first heard people talk about “pay yourself first,” it sounded like a cute slogan. Then I ran the math.

When the U.S. Securities and Exchange Commission explains compound interest, they give examples like this: if you invest $100 a month at a 7% average annual return starting at age 25, you can end up with around $250,000 by age 65. If you wait until 35 to start, you’d have about half that, even though you contribute for 10 fewer years. That’s the power of small, consistent moves, not one big heroic act.

I used to think, “Well, I can’t put away $500 this month, so what’s the point?” The real shift happened when I started treating $20 like it mattered. Over a year, $20 a week is more than $1,000. Put that into a 4–5% APY high‑yield savings account (which many online banks genuinely offer now), and your emergency fund stops being a sad intention and starts becoming a real thing.

In my experience, the trick is automation with a manual override:

- I set small automatic transfers (like $25 every Friday into savings).

- During Money Sunday, I decide if I can afford to add more that week or need to pause.

That keeps me moving forward without feeling trapped.

What This Routine Fixed (And What It Definitely Didn’t)

I’m not gonna pretend a weekly ritual solved everything. It didn’t magically erase my student loans or make housing any less ridiculous. But here’s what it did do within about 3–6 months:

Huge wins I actually saw:- No more overdrafts. I haven’t paid an overdraft fee since I started. Before, I’d get hit a few times a year because I was winging it.

- Credit card chaos turned into a plan. I listed my balances by interest rate and used a hybrid of the “avalanche” method (highest interest first) with a tiny “snowball” win (one small card paid off fast for motivation).

- I built a real emergency buffer. I went from “uhh, I think I have $200 somewhere?” to three full months of bare‑bones expenses in a high‑yield savings account. That felt like breathing for the first time in years.

- Money stopped feeling like a scary mystery. I don’t love every number I see, but I’m not in the dark anymore.

- Income problems. If your income doesn’t cover basic needs, no level of “Money Sunday” can fully solve that. It can help you see the gap clearly and make better decisions, but it’s not a substitute for higher pay, more hours, or a new gig.

- Structural issues. High rent, healthcare costs, student debt policies—those are systemic. A routine doesn’t erase them, though it can help you navigate them a bit more strategically.

- Impulse control 100% of the time. I still make dumb purchases sometimes. The difference is I catch them faster and learn from the pattern.

I want to be honest: this routine is powerful because it’s boring and repeatable, not because it’s glamorous. There’s no hack, no crypto lottery, no “secret credit trick banks don’t want you to know.” It’s you, your numbers, once a week, with a bit of honesty.

How to Start Your Own “Money Sunday” Without Overcomplicating It

If you want to try this, here’s the version I wish I started with—lightweight and judgment‑free.

For the first four weeks, keep it insanely simple:

1. Pick your time and place.I do Sunday evenings with a drink (coffee, tea, wine—no judgment) and music on. Same couch, same vibe. Consistency matters more than perfection.

2. Use what you already have.You don’t need fancy software. Start with:

- Your banking apps

- A notes app or Google Doc

- A calculator on your phone

If you like apps, cool. If not, don’t let that be the barrier.

3. Follow this loose script:- “What’s my checking + credit card situation right now?”

- “What surprised me this week?”

- “What’s coming up next week that costs money?”

- “What one tiny move can I make for Future Me?”

The first month might be rough. You’ll see stuff you’d rather not see. Instead of spiraling, treat yourself like a scientist: “Oh, interesting, that’s where it’s going.” Data, not drama.

When I did this for one month, I mostly just felt exposed. By month two, I started to feel more in control. By month three, I could literally predict my stress levels based on whether I’d done the routine or skipped it.

And that’s the thing: this is less about perfect money decisions and more about building a tiny weekly checkpoint so your finances aren’t a black box.

If you try it, customize it hard. Maybe you do “Money Monday” before work, or “Finance Friday” at lunch. Maybe your tiny wealth move is calling your internet company once a month to negotiate (I’ve done this—got $20/month knocked off a bill with one 15‑minute call). The specific shape doesn’t matter; the weekly rhythm does.

Conclusion

When I finally treated my money like something I should hang out with weekly instead of a monster under the bed, everything shifted. Not overnight. Not dramatically. But steadily, like turning a steering wheel a few degrees and realizing a mile later you’re in a completely different lane.

A weekly “Money Sunday” won’t fix an unfair economy, but it will give you back a sense of agency. You stop getting blindsided. You start pre‑deciding. You build these tiny, boring habits that quietly stack into actual financial stability.

And the weirdest part? After a while, it stops feeling like “doing finances” and starts feeling like checking in with a future version of you that’s genuinely grateful you showed up for an hour once a week.

If you end up building your own version of this, screenshot your setup, tag it, share it. People don’t need more money shame; they need more “hey, here’s the small thing I’m doing that actually helped.”

Future You is watching. Give them something to work with.

Sources

- U.S. Securities and Exchange Commission – Investor.gov: Compound Interest Calculator – Explains how small, regular investments grow over time and provides examples and tools to run your own numbers.

- Consumer Financial Protection Bureau – Credit Card Fraud Protection – Details how fraud happens, how to spot suspicious charges, and what to do if you find them in your weekly review.

- Federal Trade Commission – Consumer Sentinel Network Data Book – Offers data on fraud and identity theft reports in the U.S., including trends in credit card fraud over the years.

- Federal Reserve – Report on the Economic Well-Being of U.S. Households – Provides statistics on Americans’ savings, emergency funds, and financial stress, giving context to why routines like weekly check-ins matter.

- Morningstar – The Case for Low-Cost Index-Fund Investing – Explains why low-cost index funds are a common recommendation for long-term investing and how fees impact returns.