The “Broke But Investing” Playbook: How I Built a Portfolio on Less Than $50 a Week

I used to think investing was something you started after you were “good with money.” Stable job, no debt, six months of expenses saved, a color‑coded budget spreadsheet… all the things I absolutely did not have.

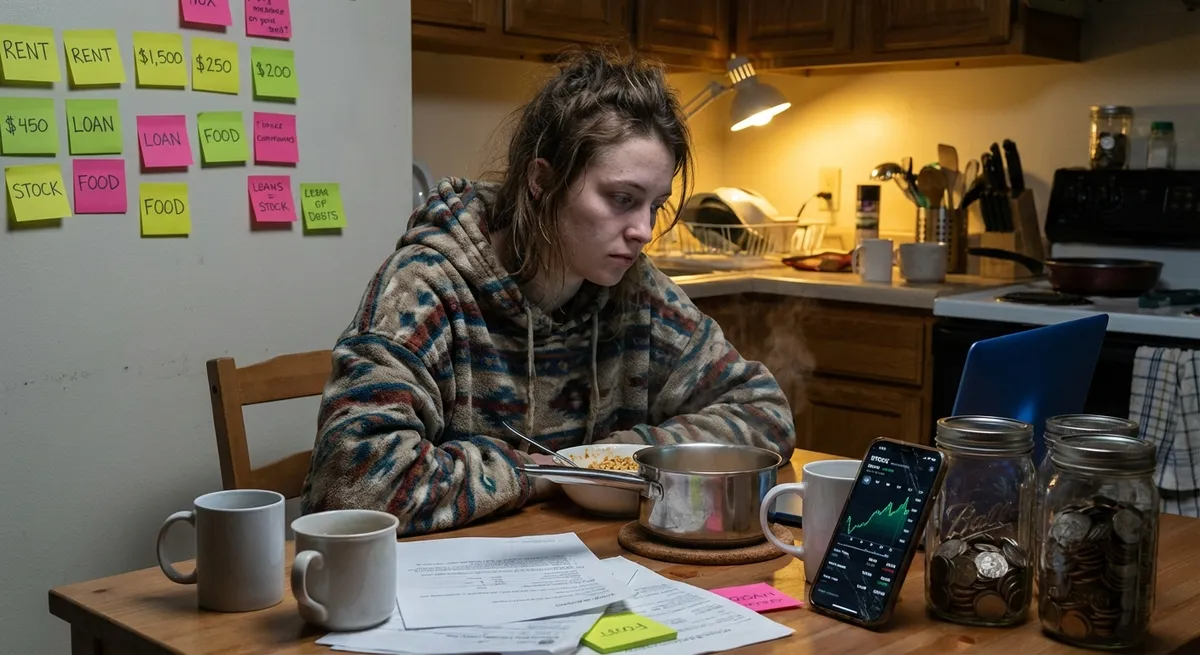

What I did have? A checking account that was constantly flirting with overdraft fees, a credit card bill that made me sweat, and about $40–$60 each week that somehow disappeared into takeout, impulse Target runs, and “emergencies” that were really just poor planning.

When I finally got serious, I decided to see if I could build a real investment portfolio on less than $50 a week without becoming a full-time finance robot. No lottery wins. No crypto YOLOs. Just boring, repeatable steps.

Here’s exactly how I did it—and how you can steal the playbook.

How I Went From “I’ll Invest Later” to Actually Owning Stuff

The turning point was hilariously small: $10.

I downloaded a brokerage app because they were offering a $10 sign-up bonus. I started with fractional shares because I couldn’t afford a full share of anything decent. When I bought my first $5 slice of an S&P 500 index fund, I expected… nothing.

But one month later, that $5 was $5.23. Twenty‑three cents. It’s ridiculous how motivated I got over twenty‑three cents.

That tiny win did two things for me:

- It proved the market wasn’t some locked VIP room for rich people.

- It made me way more protective of the money I wasn’t investing. I’d stare at a $12 DoorDash fee and think, “That’s almost three days of investing.”

From there, I started tracking just three numbers every week:

- How much cash I actually had left on Sunday

- How much went to high‑interest debt

- How much I pushed into investments, even if it was $5

No fancy app. I literally wrote it in my phone’s Notes app. Once I could see the numbers, the stress got quieter—and the investing habit got stickier.

The Micro-Investing Blueprint I Used (and Still Use)

When I tested different strategies, the stuff that looked exciting on TikTok usually blew up in my face. Meme stocks, options, hot stock tips from that one guy on YouTube—I tried a few, lost money, and got humble very quickly.

What ended up working was extremely boring:

- Automated transfers as small as $10–$25 per week into a low-cost brokerage account

- Fractional shares of broad index funds instead of individual “lottery ticket” stocks

- A simple rule: Don’t invest money you need in the next 3–5 years

When I set up a $20 weekly auto-transfer, I didn’t feel it as much as I expected. I felt it way less than a random brunch, but it slowly grew into real money.

To give you an idea of how this can add up:

- Historically, the S&P 500 has returned around 10% annually before inflation over long periods (1926–2023 range) according to data summarized by NYU Stern’s Aswath Damodaran and others. That doesn’t mean every year is good—far from it—but the average has been strong.

- If you invest just $50 per week (about $200/month) at an average 8% annual return over 20 years, you’re looking at roughly $118,000+. That’s not “I retired at 29” money, but it is life‑changing “I have options” money.

The key thing I learned: the habit matters more than the dollar amount at the beginning. I started at $10 some weeks when money was tight. What mattered was not breaking the streak.

Where My Money Actually Goes (And Why I Stopped Chasing Hot Tips)

I used to think I had to “beat the market” to get ahead. Then I looked at the numbers.

A famous study from S&P Dow Jones Indices (the SPIVA reports) shows that most actively managed funds underperform their benchmarks over 10–15 year periods. Translation: a lot of highly paid professionals can’t reliably beat a plain old index fund that just tracks the market.

Once I accepted that, my approach simplified fast:

- Core holding: A broad U.S. stock market index fund or S&P 500 index fund (like VTI, VOO, or similar from different providers). These hold hundreds of companies, giving built-in diversification.

- Optional spice: A small slice in an international index fund and a bond fund as I got more stable financially.

- Avoiding noise: I stopped checking my portfolio daily. When I tested doing that, I made emotional decisions—selling low, buying random stuff. Now I try to check once a week at most.

There are pros and cons to this “boring index” approach:

Pros:- Very low fees (expense ratios often under 0.10%)

- You’re spread across many companies, so one disaster doesn’t wreck you

- Historically strong returns over long periods, even with recessions mixed in

- No bragging rights—your friends with that one lucky stock pick might look richer short term

- You have to be okay with big drops some years (like 2008 or 2022) and keep going

- It feels slow and unexciting when social media is yelling about 200% gains in a week

But when I compared the quiet, steady growth of my index funds to the emotional rollercoaster of my “fun” picks, the winner was obvious.

Balancing Debt, Bills, and Investing Without Losing Your Mind

Here’s the part nobody on finance TikTok wanted to talk about: I had ugly debt.

For a while, I tried to invest and make only minimum payments on a credit card charging over 20% interest. That was a mistake. When I did the math, it was painfully clear: putting extra money into a high‑interest card was a guaranteed 20% “return,” which beats any realistic stock market expectation.

So I shifted my approach:

- Anything above ~15–20% interest (like many credit cards) got priority. I attacked those balances while still doing teeny-tiny “symbolic” investments, like $5 a week, just to keep the habit.

- Lower-interest debt (like some student loans or car loans around 4–6%) became more of a balancing act. I’d split extra cash between additional payments and investing.

- I kept a small emergency buffer—even just $300–$500—because when I didn’t, I’d swipe my card every time life happened, and the whole cycle restarted.

One practical thing that changed my life: I turned my budget into “jobs” instead of just numbers.

Example of a broke-but-trying week:

- $20 – Minimum payments on all debt (non‑negotiable)

- $15 – Extra payment toward the highest-interest debt

- $10 – Automatic transfer to investments

- Whatever was left – groceries, gas, tiny fun

Was it perfect? Absolutely not. Some weeks the “extra payment” became “my car needed a tire.” But having that structure stopped me from drifting back into pure survival mode.

How I Avoided the Biggest Beginner Money Traps

When I first started, I fell face-first into several classic traps. If I can save you from even one of these, I’ve done my job.

Trap 1: Confusing investing with gamblingWhen I chased hype stocks and random coins “to the moon,” I wasn’t investing—I was speculating. I had no thesis, no plan, just adrenaline. Now, if I can’t explain in one sentence why I own something, I don’t buy it.

Trap 2: Ignoring feesI once owned a mutual fund with a 1.2% expense ratio because a bank rep said it was “solid.” After I did some reading, I realized that paying 1%+ every year in fees can cost you tens of thousands over decades. I switched to low-cost index ETFs with much smaller expense ratios and kept more of my own returns.

Trap 3: Trying to time the market perfectlyI waited for “the crash” to start investing. Then the market went up. Then I waited again. Eventually I realized the pros can’t consistently time the market either. So I switched to dollar‑cost averaging—investing the same amount every week regardless of the headlines. When I tested that for 12 months, I ended up buying more shares when prices were lower without even trying.

Trap 4: Comparing my Chapter 1 to someone else’s Chapter 20I’d see people posting their $200,000 portfolios and feel like my $1,500 was a joke. It wasn’t. That $1,500 was the hardest money I’ve ever invested, because I did it when I had the least. Once I reframed it that way, I stopped trash‑talking my progress.

When Investing on a Tiny Budget Doesn’t Make Sense

I’m obviously pro‑investing, but there are times where, in my experience, it’s better to pause or go minimal:

- You’re constantly paying overdraft fees or bouncing bills

- You have no emergency buffer and any hiccup sends you straight to high‑interest debt

- You’re battling payday loans or credit cards with sky‑high APRs

- You’re not sleeping at night because you feel overextended

In those seasons, I’ve done “maintenance mode”: $5 a week just to keep my head in the game while I bulldozed the crisis stuff. Investing shouldn’t feel like self-punishment or a guilt trip. It’s a tool, not a virtue signal.

The goal isn’t to be the perfect investor—it’s to be the version of you that has more choices 5, 10, 20 years from now.

The Part That Actually Changed My Life (Not the Dollar Amount)

The weirdest surprise of all this? The actual money was only half the reward.

By forcing myself to invest something every week, I accidentally rewired my brain from “I’m bad with money” to “I’m someone who builds things slowly.” That identity shift made it easier to:

- Say no to random spending because I had a specific “yes” (future me)

- Negotiate a raise, because I now saw extra income as rocket fuel, not just survival money

- Talk about money openly with friends and family without shame

When I look at my portfolio now, it doesn’t scream “genius investor.” It whispers, “You showed up. Even when it sucked. Even when it was $10.”

If you’re reading this while your bank account looks depressing and your debt feels like a weighted blanket made of bricks, here’s what I’d do if I were starting over today:

- Open a low-fee brokerage account that allows fractional shares

- Automate the smallest weekly transfer you won’t cancel—$5, $10, $25

- Put it into a broad, low-cost index fund you understand

- Attack any soul‑crushing high-interest debt in parallel

- Focus on streaks, not perfection

You don’t need to be rich to start investing. You need to start investing to eventually stop feeling broke forever.

And yes, even if it’s just $10 this week.

Sources

- U.S. Securities and Exchange Commission – Beginner’s Guide to Asset Allocation, Diversification, and Rebalancing – Clear explanation of diversification, risk, and long‑term investing basics

- FINRA – Dollar-Cost Averaging – Covers how investing a fixed amount regularly can help manage market volatility

- S&P Dow Jones Indices – SPIVA U.S. Scorecard – Data showing how many active funds underperform their benchmarks over time

- NYU Stern (Aswath Damodaran) – Historical Returns on Stocks, Bonds, and Bills – Long‑term data behind average stock market returns

- Consumer Financial Protection Bureau – Credit Card Interest and Fees – Explains how high‑interest debt works and why it can be so costly